To listen to an audio spoken phrase model of this publish, click on right here.

All people appears to be having a tough time with the phrase “Transitory.” A part of that is because of the approach individuals expertise time within the fashionable period. Maybe it might be useful to reframe this otherwise, utilizing a much less temporal method.

Take into account this query: Are rising costs a “Structural” a part of the economic system? Are they a everlasting fixture, a part of the outlook for the price of items and providers for the subsequent decade or longer? If we’re to dismiss “Transitory,” then we should, by definition, embrace inflation as “Structural.”

I don’t see this in a lot of the largest value will increase — they don’t seem to be everlasting components of the economic system. It is because — Warning: priors forward! — the dominant value impetus the previous three a long time has been technology-induced Deflation. The more moderen drivers of Inflation all seem like pandemic/re-opening/provide chain pushed, and due to this fact not structural.

Take into account among the larger parts of the current file excessive CPI:

• Cars (new and used): One of many largest drivers of upper costs has been the auto sector, though they’re solely 7.8% of total consumption (new autos = 3.83%; used = 3.29%). From March 2020 to August 2021, used automotive and truck costs have gone up 43.3% versus 11.7% for brand spanking new autos versus U.S. inflation price of seven.3% (at present 6.2%). That is clearly a re-opening problem brought on by the semiconductor provide issues, not a structural change in automotive costs.

There are indicators this has peaked and is abating: The CEO of Ford mentioned the semiconductor scarcity is bettering however will lengthen into subsequent yr (September); the CEO of Volkswagen mentioned we have now “seen the worst” of the chip scarcity (October); Toyota introduced manufacturing strains in Japan are scheduled to function usually for the primary time in seven months (November). And final week, Morgan Stanley analysis famous chip manufacturing in Malaysia returned to full manufacturing; they anticipate automotive manufacturing (and chip intensive customers like cloud knowledge heart servers) to enhance within the close to future.

The entire above is why costs for cars ought to start to start out normalizing in Q1 or Q2 2022. That is exactly what transitory inflation is versus structural inflation.

• Shelter: One of many largest parts of inflation knowledge is Shelter at 41.7% of CPI. This contains owned properties and leases. The complication is there are over 95 million owned properties in America, about 2/3rds of that are owner-occupied. About 6 million of those change palms every year.

It’s a difficult side of CPI: Housing has been disrupted by the low numbers of properties constructed within the years after the monetary disaster; it was exasperated by the surge of city dwellers in search of alternate options to cramped residences throughout covid lockdowns.

And the so-called dying of cities wasn’t merely exaggerated, it was lifeless mistaken. Renters have returned to cities in giant numbers, and the 2020 slashed hire costs we noticed are returning to regular or above. A part of that large enhance in rents is the unfavorable year-over-year comparables to the pandemic hire lows (and eviction moratorium). It will possible kind itself out over the subsequent few quarters.

These are the transitory components of Shelter pricing, however different elements of residence costs are certainly structural: think about New Dwelling Building and modifications to state and native rules that forestall larger density land use. The excellent news is that new housing models below development at the moment are on the highest stage since 1974; we should always harbor no such phantasm concerning the imminent elimination of NIMBYism anytime quickly.

• Wages: The first driver of rising wages has been the underside half, specifically the backside quartile. That is the place compensation has lagged for many years and is now catching up. As famous yesterday, Actual Median Wages had been unchanged from 1979 to 2014; Actual Minimal wages had been the identical in 2015 as they had been in 1949.

What is happening on the backside of the wage scale is an enormous unwind of a long time of wages that had been deflationary in nature. I anticipate these will increase will probably be sticky, however the annualized positive aspects will average. Therefore, one of the best ways to think about backside half wages as a part of a nice reset.

We do have a supply-constrained labor drive, due partially to diminished immigration, early retirements, employees leaving dead-end industries, lack of kid care, and Covid deaths. That is contributing partially to these rising wages.

• Vitality: Rose about 30% over the previous yr; this part is 7.3% of CPI. A few of that is supply-driven, however Vitality has a number of cross-currents occurring inside it: Costs fell after the 2008-09 disaster; that diminished the inducement for capital intensive fracking, which helped restrict provide. There are some indicators we’ll see extra fracking in 2022.

The structural portion of that is the transfer from carbon to inexperienced vitality. That social choice helps to drive the costs of different vitality decrease. Photo voltaic, wind, and geothermal are nonetheless comparatively small parts of whole vitality consumption, however they’re rising. And, they’re a expertise not commodity -based vitality supply. They’ve the potential to be deflationary, not inflationary.

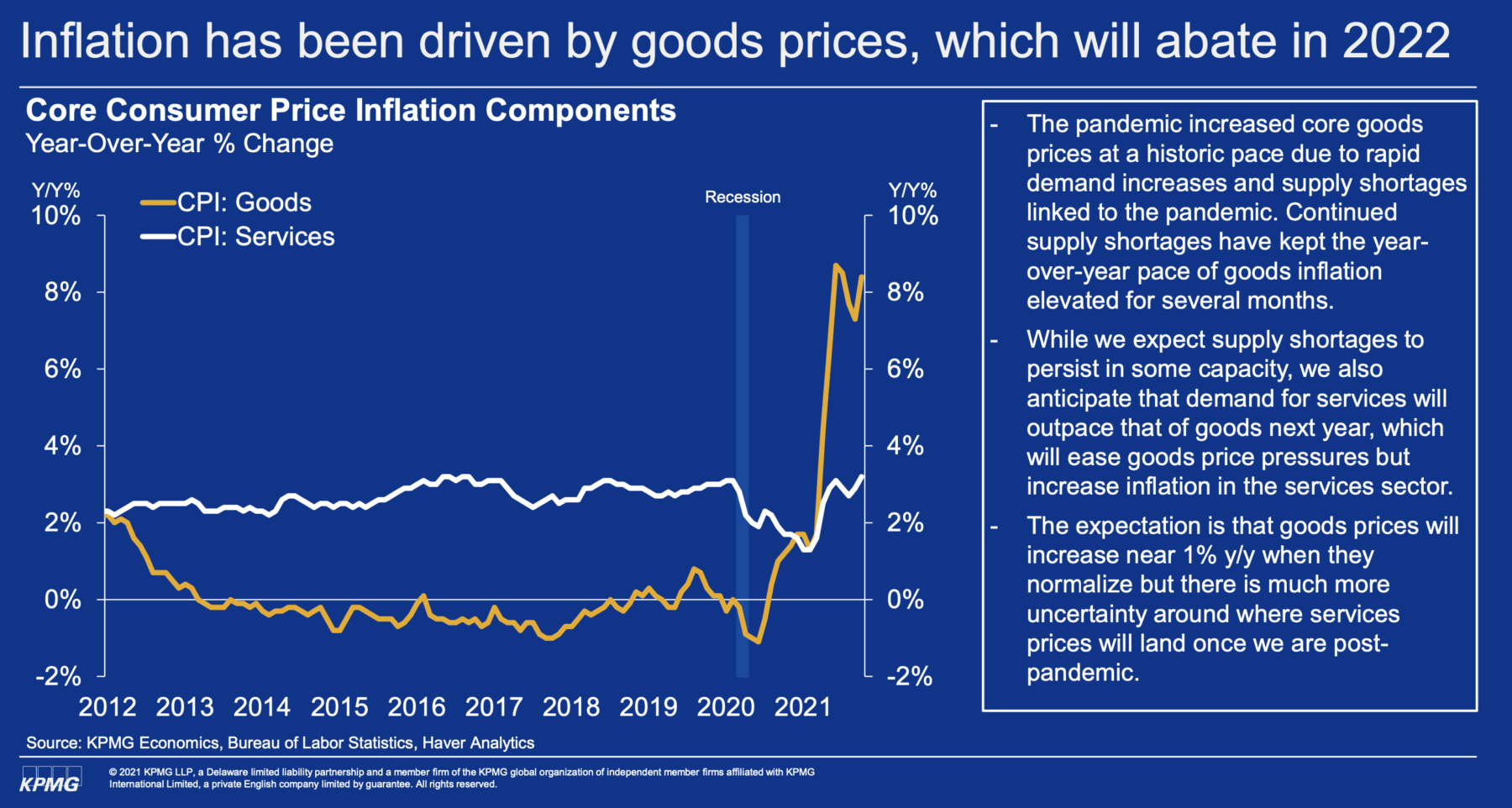

• Items versus Providers: Final, think about the steadiness between bought Items (38.7%) versus consumed Providers (61.3%): As our chart exhibits, it’s not the service economic system driving rising costs, however quite the products portion of the equation. CPI Items are up over 8%, whereas CPI Providers have recovered again to the place they had been pre covid — at about ~3% value will increase.

It is a enormous component within the inflation dialogue.

Why? A part of that is pushed by the modifications that occurred in the course of the pandemic lockdown, and that was a transfer in the direction of items and away from providers. As an economic system, we out of the blue started shopping for meals through Instacart/Amazon as an alternative of going out to eat; we purchased Peletons vs a fitness center membership; we bought giant display screen TVs as an alternative of going to the flicks; we purchased vehicles and Winnebagos as an alternative of happening trip.

In every of those cases, you bought a bodily good as an alternative of utilizing a service — and did so in portions far outdoors of what’s usually bought. That is the alternative of the pre-pandemic development. That the provision chain buckled below the load isn’t a shock.

~~~

Costs have risen in lots of areas, and the query is whether or not the annualized price of enhance will keep excessive, or fall again to regular, from these elevated ranges. I think we’re two-thirds by a reset in costs, a lot of which is able to show sticky, however are unlikely to proceed at these elevated charges of change.

Low-end wages gained’t return to pre-pandemic ranges, however used automotive costs and gasoline will; “Aspirational” single-family residence costs are more likely to go away as extra provide comes on-line from new development and extra individuals promoting their present properties. Leases are again in lots of locations to pre-Covid ranges, however the provide shock is perhaps a considerable conversion of overbuilt workplace area to residential utilization.

Lots of the present costs we see are the “new regular,” however a lot of the present annualized price of enhance isn’t.

Beforehand:

How We Expertise Time, Inflation Version (November 10, 2021)

How All people Miscalculated Housing Demand (July 29, 2021)

Deflation, Punctuated by Spasms of Inflation (June 11, 2021)

Elvis (Your Waiter) Has Left the Constructing (July 9, 2021)

The Inflation Reset (June 1, 2021)

Shifting Stability of Energy? (April 16, 2021)

click on for audio

The post Structural or Transitory? – The Massive Image appeared first on TheBestEntrepreneurship.

source https://thebestentrepreneurship.com/structural-or-transitory-the-massive-image/

No comments:

Post a Comment